Hey there savvy savers!

It’s Emma, your go-to girl for all things finance and… cooking? That’s right! Today, we’re dishing out lessons from my kitchen that surprisingly reminded me of the principles of smart investing. My trusty air fryer, beyond serving up the absolute crispiest potatoes, turned out to be an unexpected teacher in the importance of consistency, both in the kitchen and in my investing journey with saveday.

Cooking Up Savings with the Air Fryer

My mom is an air-fryer-evangelist. She taught me all about how it could whip up healthier meals without excess oil. But when I started, much like diving into a new investment, I was both excited and skeptical. Yet as I experimented, a pattern emerged. The consistent heat circulation ensured that my dishes were cooked perfectly every time. No more soggy centers or burnt edges; just golden-brown perfection, bite after bite.

Moreover, consistently using the air fryer made me realize the savings I was racking up. Fewer dining-out expenses and reduced grocery bills (since I wasn’t wasting ingredients on my botched cooking experiments) were clear indicators of how consistency pays off.

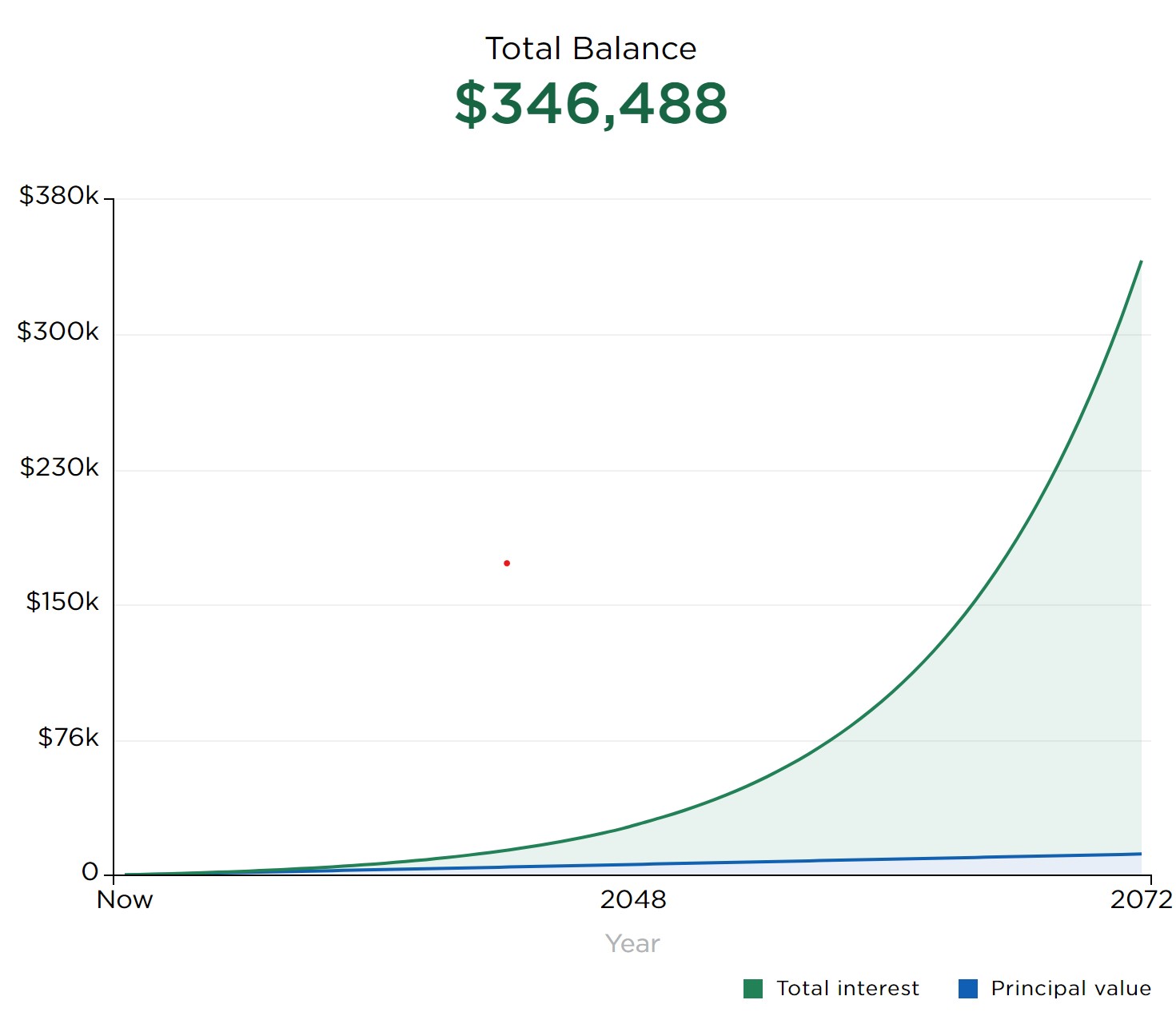

The Parallel World of Investing

This got me thinking about my finance journey. Just as the steady circulation of the air fryer leads to optimal cooking, consistent investing with saveday helps optimize my financial growth. For me, it’s not about throwing all your money in at once or investing sporadically. It’s about the commitment to a regular, disciplined approach that yields results over time. Just take a look at how much a consistent $5 a week can grow over time.

Graph Generated by Nerdwallet

When you partner with saveday for your 401(k) plans, think of it as setting the temperature on your air fryer. You’re laying down the groundwork for a recipe that, with time and consistency, will provide delectable returns.

Small Inputs, Compounding Outcomes

With my air fryer, small, consistent actions— like preheating, using minimal oil, or setting the timer— translated to mouth-watering meals every time. Similarly, in the realm of finance, regular contributions to your savings or 401(k) can lead to substantial growth over time, thanks to the magic of compound interest.

Consistency Over Time is Key

Just as you wouldn’t crank up the heat on your air fryer hoping to get quicker results (spoiler: like me, you’ll probably just burn your food), it’s essential not to seek shortcuts in investing. Instead, setting a consistent contribution rate and sticking to it, irrespective of market highs or lows, is a strategy that often proves successful in the long run.

Concluding Bites

In the end, my air fryer taught me that whether you’re cooking up crispy fries or a secure financial future, consistency is your best ally. By maintaining a disciplined approach, being patient, and understanding the process, you can ensure that your investments, much like your meals, turn out just right.

For more tips on mastering the art of saving, read on here!

Yours in flavor and finance,

-Emma